A sector under siege from a wave of FinTech disruption is gearing up for the battle by embracing the digital technologies being deployed against them.

Key insights:

Understanding and responding to the threat of FinTech disruption

Blockchain and other major technological trends

Pathways to Innovation

SaaS – bridging the gap to Micro Business Services

Streamlined enterprise communications – programmatically transforming business capabilities

Operational communications in action

It’s commonly accepted by the leaders of financial institutions that the same technological changes that have disrupted industries from media to books, retail, and advertising are poised to fundamentally change the banking & finance sector.

Industry leaders estimate that as much as 23% of their revenue is at threat by 2020, from nimbler tech native startups targeting the most lucrative parts of their businesses.

Cutting costs or increasing digital marketing budgets isn’t enough. Institutions are responding by embracing the technologies being deployed against them, as they attempt to adapt by transforming operating models, and forming creative partnerships with tech partners who can rapidly supply new capabilities.

Industry leaders estimate that 23% of their revenue is at threat from FinTech startups

Global investment in FinTech reached nearly $13.8bn in 2015, Up from just $2.1bn in 2011

SaaS software spending forecasted to grow 21% over 2015 spending levels

80% of institutions are planning to leverage mobile for operational communications

Executive summary:

The banking and finance sector is facing the same technology-driven competitive pressures that have disrupted other industries from books to music, retail, and advertising, which have seen as much as 50% of their revenues decimated in recent years.

For financial institutions this is embodied by the growth of FinTech – an industry filled with nimble, technology-based competitors, targeting the most pro table parts of their businesses. Venture capital support for the industry is growing fast - global investment in FinTech startups reached nearly $14bil in 2015, up from just $2.1bil 2011, arming them with the war chests to effectively take the fight to larger, established organizations.

Banks are also having to adapt to digital, mobile, and internet-inspired changes to customer preferences, in both emerging and developed markets; as well as learn how to embrace revolutionary technologies like Blockchain, that have the potential to transform banking operations.

Incumbents believe that 23% of their business is at risk if they can’t embrace innovation in time to stave off the competition.

Investing in innovation:

While there’s no one size fits all approach to adopting new technologies, three of the key paths institutions are actively exploring include:

Investing in the competition: Creating their own fintech divisions, and also investing directly in complementary tech startups;

Investing in the development: Adopting new software development practices, such as Microservices, to bring new products to market faster;

Investing in capabilities: Buying in functionality, especially software-as-a-service (SaaS) solutions that can be easily, quickly, and affordably integrated to improve and simplify operations.

Streamlined enterprise communications:

SaaS communication suites allow institutions to digitize and move messaging processes away from high-cost, inefficient channels, and mass notifications, to information tailored to the needs of the audience.

This offers dramatic operational improvements in areas including:

Strategic IT service management

More efficient notifications free up staff resources and allow IT to more effectively support an innovation agenda.

Internal operational communications

Workforce management for a wide range of functional areas such as company announcements, IT system updates, sending account authentication and password reset information, timesheet processing, and shift fulfillment.

Customer journey management

Automating and digitizing customers’ digital touchpoints in areas such as onboarding, service, support, billing, and collections.

Programmatic workflow reimagination

SaaS deployed capabilities can be adopted with no development lead time, and allow existing workflows to be rapidly redesigned and improved.

Modern communication suites can be integrated with existing internal and customer-facing systems, leveraging their functionality and data to rethink and automate traditional business processes, creating the foundation for effective operational innovation.

Changing competitive landscape:

The growth of accessible cloud infrastructure, SaaS and open source software solutions, and mobile computing, has significantly lowered barriers to innovation, distribution, and adoption of IT. This ubiquitous access to advanced technology is seeing software and digital communications technology becoming key differentiators in the way that organizations of all sizes now compete.

More and more major businesses and industries are being run on software and delivered as online services— drawing inspiration from Silicon Valley-style entrepreneurial technology companies that are rapidly disrupting established industry structures.

Disruption tipping point:

Software disruption typically manifests when nearly 50% of the incumbent revenue is lost to technological competition. In less than two decades, the global recorded music industry has lost over half its revenues, while the drop in newspaper advertising revenues has been even steeper.

Video streaming, advertising, media, music, books, and retail are all examples of industries that have been fundamentally disrupted by technology.

The banking and financial sector is facing disruption from a range of sweeping technological forces, including FinTech competition; rapidly changing customer expectations of service and access; and emerging technologies, such as Blockchain.

Fintech:

Financial Technology, or FinTech, is an economic industry comprised of technology-based startups aimed at innovation in financial services, and targeting the most profitable parts of the business of incumbents in the banking and financial sector.

Global investment is firmly recognizing the potential for this market, with FinTech funding reaching nearly $14bil in 2015, up from just $2.1bil 2011.

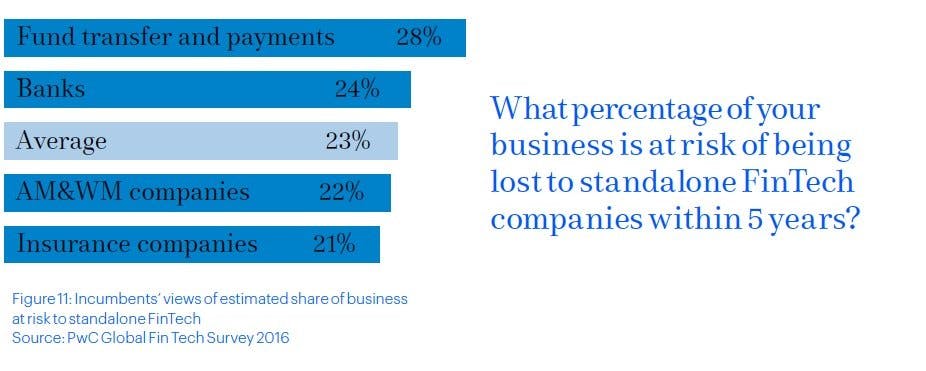

PwC’s 2016 Global FinTech Report shows the vast majority (83%) of respondents from traditional Financial Institutions believe that part of their business is at risk of being lost to standalone FinTech companies. Incumbents believe that 23% of their business could be at risk, while FinTech companies are actually targeting a 33% market share.

In response, banks are attempting to maintain profitability by lowering costs and improving operations through an increased pace of technology innovation.

Cost reduction measures are typically in customer-facing headcount, with branch staffing reductions aligned to changing preferences for increased digital transactions, and decreased demand for cash.

In the U.S, for example, branch numbers have dropped from a peak of 95,000, down to 86,000 branches, and are expected to drop to around 75,000 within 3 to 5 years.

Transforming access to financial services:

Technology is opening access to banking services in emerging markets, and changing the expectations that customers have for interacting with banks, especially in the demand for improved payment processes.

Developing world – mobile-first access to banking:

Access to mobile banking is allowing much of the developing world to bypass traditional financial infrastructure altogether, especially in regions where no physical banking access has previously been possible.

Tanzania, for example, has 10 times as many mobile money agents as all other financial intermediaries. Neighboring Kenya is a leader in phone-based financial services since developing the M-PESA mobile payments system in 2007, which currently has 23 million active customers in 11 countries.

Sweden, Denmark moving to a cashless society:

Sweden provides a compelling illustration of the move towards a cash-free future, in a society where bills and coins now represent just 2 percent of Sweden’s economy, compared with 7.7 percent in the United States and 10 percent in the euro area.

In 2015, only about 20 percent of all consumer payments in Sweden were in cash, vs an average of 75 percent in the rest of the world.

Many Swedish bank branches no longer hold cash, and payments are mostly facilitated by electronic transfer and mobile applications, such as the Swish direct payment app, a collaboration between major Swedish and Danish banks, allowing transactions between individuals, in real-time.

Blockchain:

Blockchain was originally introduced by Satoshi Nakamoto in 2008 as the distributed ledger technology securely recording every bitcoin transaction that has ever occurred. As the ledger is distributed and shared amongst many parties, the information held is easier to verify, and it becomes cheaper to transact between parties, with the removal of process intermediaries.

Blockchain has transformative potential for many industries, as seen by the rapid increase in equity investment in the segment - growing to $454 million in 2015, up 500% in just 2 years. In 2015 a consortium of 9 leading global banks including JP Morgan Chase, UBS, Barclays, and the Commonwealth Bank of Australia joined forces to actively collaborate on finding potential applications for Blockchain technology. Early examples include:

Back office processing, such as improving the speed, and lowering the costs of clearinghouse functions between banks

Smart contracts are automatically settled as soon as the terms are executed. This can include payment settlement, or digital repossessions, such as shutting down a car electronically if loan payments are not made

Self-executing securities – e.g bonds that automatically pay the coupons to bondholders upon maturity, without any need for human intervention

While Blockchain potential is now beyond question, how to actually use the technology is a clear limiting factor. PwC’s Fin-tech Report shows that the majority of respondents (56%) recognize its importance, but 57% say they are unsure or unlikely to respond to this trend.

This is likely due to the low level of familiarity with this new technology - 83% of respondents are at best “moderately” familiar with it, which places market participants at risk of underestimating the potential impact of blockchain on their business.

Investing in innovation:

The 2015 BCG retail banking excellence (Rebex) study showed that banks leading in measures of operational and digital excellence are achieving 50% higher average profit per customer, and 30% lower operating expenses per customer - largely driven by lower personnel and IT costs.

Banks are investing heavily in new technologies to streamline operations, in response, but spending money alone isn’t a clear solution - banks have always invested heavily in technology – in 2015 total bank IT spending across North America, Europe, and Asia-Pacific grew to $196.7 billion.

The challenge is the time, difficulty, and resources required to create and integrate new enterprise technologies. A nimbler approach is needed to embrace innovation at the pace of their leaner FinTech competitors.

Three of the key paths being explored to actively embrace technological innovation include:

Investing in the competition: Banks have begun to see fintech companies as potential enablers, rather than simply as competitors, creating their own fin-tech divisions, and also investing directly in complementary tech startups. Corporate participation in Venture Capital-backed fin-tech companies grew to 25 percent of total sector investment in 2015.

Investing in development: Adoption of new software development practices, such as Microservices, which offer increased agility, allowing them to bring products to market faster while navigating the inherent risk attached to the speed of deployment. The National Australia Bank (NAB) recently discussed the role of Microservices in allowing them to innovate and compete in the burgeoning FinTech arena. Instead of needing months or years to develop new features, NAB is able to implement a layered approach that isolates their core banking system (now exposed via an API) while also allowing them to build and update services quickly while managing the accompanying development risk.

Investing in capabilities: PWC asserts that Solutions that banks can easily integrate to improve and simplify operations are most important for maintaining competitiveness. Open development and software-as-a-service (SaaS) solutions are critical to giving banks the ability to rapidly streamline operational capabilities.

SaaS – bridging the gap to micro-business services

For many organizations, redesigning their software engineering teams and practices is a complex, time-consuming and risky endeavor, leading to the growth of Software-as-a-service (SaaS) as a means of rapidly deploying new application services or functionality.

SaaS vendors typically specialize in developing and maintaining discrete, best-in-breed software, which can easily be integrated into existing bank platforms, and are constantly upgraded, without the need for investment in the requisite research, design, and development of new technologies.

Streamlined enterprise communications

SaaS-based communications suites can be rapidly adopted, allowing banks to digitize and move messaging processes away from high-cost, inefficient channels and methods, such as connecting to Collections software and contacting customers via automated SMS, rather than manual calls.

Institutions are moving from mass notifications that struggle to generate cut-through, to tailored information, targeted appropriately to the audience, designed to inspire action and avoid messaging fatigue.

Modern digital platforms with communication suites can help fuel an innovation agenda by streamlining a range of operational communications, and programmatically transforming the underlying business processes.

Strategic IT service management communications

In order to support an innovation agenda, studies suggest that no more than 50% of IT spending should be on activities whose sole purpose is to prevent existing systems from breaking down. For most companies, however, the average is around 72%, with only 28% of the IT budget going toward new projects.

Existing manual processes absorb a significant portion of IT staff resources. A major issue is the overwhelming deluge of notifications flooding into the inbox of IT staff every day, exceeding notifications 100,000 per day in the larger organization - from basic updates to maintenance reports and outage warnings, creating the conditions for notification fatigue.

Modern communication systems with data analytics, connected to IT monitoring platforms, can deliver information targeted to the needs of the audience, at the appropriate time, and the device of choice. Well-structured ITSM communications can include:

Executive dashboards for easily viewed system-wide information

SMS or interactive Rich Messaging for urgent action to responders

Automated advisory notices for system users of planned outages and maintenance downtime

Self-service capabilities for staff to change their levels of notifications

Moving to message automation decreases the need for manual intervention in many of these processes, freeing up IT staff to focus on higher value-added services.

Operational communications

Mobile devices have become key for banking and financial businesses looking for better ways to engage their customers and improve operations in the digital age. 80% of all financial service companies are currently using, or plan on using SMS to communicate or interact with their customers and employees.

Mobiles provide workforce management for a range of functional areas, such as IT and Human Resources departments. Options include sending company announcements, providing updates, sending account authentication and password reset information, time-sheet processing, and critical notifications. Common examples include:

Rapid dissemination of critical OH&S updates

Efficient shift fulfillment

Remote workforce management

Providing alerts to traders to increase transactions and differentiate service levels based on constantly updated customer information

Customer journey management

Communications technology, and the digital tools that come along with it, provide a platform for financial institutions to cut costs associated with manual transactions, and automate the customer’s digital touchpoints, in areas such as:

Onboarding

Automatically providing interactive welcome and induction packs for new products and services, such as contracts and payment information details for new loans.

Service and support

Cutting manual handling costs by automating and digitizing ongoing operating contact, including:

Billing and collections

Payment notifications

VIP relationship management

Progress notifications for applications

Facilitating 2FA/one-time passwords

Claims management

Maintaining consistency of service when dealing with less favorable aspects of customer relationship management, such as the timing and clarity of debt collection or late payment reminders.

Programmatic workflow re-imagination

The concept of Business Process Re-engineering, which involves radically redesigning core business processes for dramatic productivity improvements, has been practiced for over a quarter of a century.

The challenges with this approach are typically the scale of the projects involved, and the time, resources, and skills required to effectively prosecute the change management activities.

This is the key advantage of SaaS deployed capabilities, as the appropriate solution can be adopted with no development lead time, and API integration typically allows these services to be connected rapidly and securely to existing systems, to leverage their functionality and data.

Synchronizing a SaaS Communications platform to HR data for example, and connecting the system to IT incident monitoring tools, provides a level of certainty that all staff in the enterprise can be reached in a timely way, with information relevant to their roles.

Transitioning to communication automation requires rethinking traditional business processes, proactive scenario planning, and innovation around operations and interactions with staff, suppliers, customers, and other stakeholders.

Factors to consider when planning for the adoption of communication enablement platforms include:

Proactive scenario planning

Having a clearly defined plan in place for communicating in different situations cuts down response time, improves the accuracy of contact, and ensures the right people are able to be reached in a timely manner with further information.

Multichannel messaging

Send messages to your staff and customers in the way that suits them, whether that’s voice, SMS, Social Media, Rich Messages, or email, to improve the rates of delivery. Knowing they will almost always have their mobiles close allows organizations to provide messages on all these channels. Geo-location can segment communications even further, such as providing multilingual messages appropriate to the recipient’s location or pre-defined contact preferences.

Interchangeable message templates

Message templates should be prepared with specifics that can be rapidly altered to suit the appropriate products, services, or situations being targeted, thereby saving time with pre-planned communication and response options.

Rapid communication

When urgent communication is required, SMS accelerates the speed of notification. Whereas half of all emails aren’t opened for at least six hours, the average text message is accessed within a few minutes and responded to within 30 minutes. Voice calls to mobile and fixed lines generate an even faster response and can be created to trigger automatically from the communications platform.

Scalability and consistency

Look for solutions that can be scaled not only to other operational parts of the business, but can also scale internationally, and comply with regulatory requirements in differing jurisdictions.

Unified communications

Combining all of these communication streams into a single platform, with a central reporting dashboard improves cut-through in the delivery of messages and provides a mechanism for tracking all critical communications. This allows informed, real-time decisions to be made from these conversations.

Security considerations

Financial firms face steep hurdles in meeting industry compliance requirements, and maintaining customer trust, so the adoption of any new technologies requires stringent evaluation. Vendors support and manage services, and offer SLAs which guarantee the highest levels of availability.

Data breaches can ruin the reputation of a financial organization, so any service provider must be able to guarantee the protection of personal information and financial data.

Technology partners should also be able to provide detailed references of other comparable enterprises who have conducted the necessary due diligence to firstly initiate, and then continue the relationship.

Operational communications in action

A leading global retail bank required a structured & repeatable capability for key staff to communicate with defined & targeted internal stakeholders quickly and accurately, in crisis management and business as usual scenarios.

Whispir’s Communication Platform provided integration with the bank’s HR system – with Whispir serving as a contact information and role profile database – updated nightly via an automated synchronization API. Tailored templates & distribution lists provide an accurate and self-maintaining environment for timely and efficient communication under BAU and crisis situations.

A customized staff communication Portal is provided for staff to review messages, nominate channel references and subscribe to optional messaging services. Feedback & acknowledgments from staff are designed to route through to the 24/7 Network Operations Center. SMS, email, voice, and instant teleconference Whispir capabilities are used to communicate with staff and stakeholders on a daily basis.

The result has been increased speed and efficiency of incident response teams to inform and collaborate with key stakeholders for crisis management, and information delivery best suited to the needs of operational teams.

Financial services organizations are tasked more than ever with the development and deployment of new technologies to help meet the sweeping changes to their competitive landscape.

Incorporating secure, effective systems messaging into their customer service, employee and operational communications is a conduit to the rapid transformation of organizational capabilities.

A proactive company-wide mobile messaging strategy compliant with the industry’s high standards and regulatory demands offers powerful competitive advantages through enhanced customer experience management, improved employee relations, and greater operational efficiencies.